Insights

Market Update:

Markets Adjusting to Higher for Longer

Key Points

- Expecting positive, but more modest returns ahead and greater volatility

- Sticky inflation likely to keep the Fed patient on rate cuts

- Remain focused on holding quality positions in portfolios

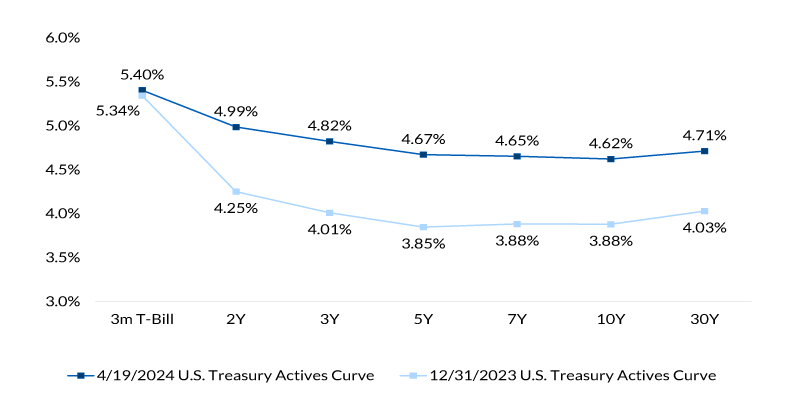

As the calendar turned to 2024, fears of a recession had faded and the U.S. economy was bound for a soft landing. Economic growth was resilient, inflation was cooling and the Federal Reserve was poised to cut interest rates, providing a catalyst for market returns. Goldilocks was back! But we would soon learn that the economy wasn’t paying attention to the speed limit. As the data rolled in, Q4 2023 GDP, inflation, retail sales and activity indexes surged above expectations, derailing hopes for rate cuts and sending U.S. Treasury yields back up to 4.7%. As luck would have it (…or not), inflation is sticky and can be volatile, reinforcing our belief in a higher-for-longer environment, and, while it appeared repricing was inevitable, the market shrugged and continued to advance on positive economic data.

Chart 1: U.S. Treasury Curve Comparison

Sources: Bloomberg, CNR Research, as of April 2024.

Information is subject to change and is not a guarantee of future results.

Our work suggests the U.S. economy is on solid footing, and we have recently lowered our risk of recession from 50% to 30%. However, growth is likely to moderate from the robust pace seen over the second half of 2023. We can’t change the laws of physics. What goes up must come down, even if this economic environment stands out for its unique ability to resist gravity. The tried-and-true methods for understanding the economy are in a serious slump, and it’s clear that high interest rates alone are insufficient to cause a recession. For now, there are no clear short-term vulnerabilities, which underpins our belief that an expansion can continue. But the same forces that power growth can put pressure on inflation, which is likely to keep rates high for longer than anticipated. This may not be the worst problem for the market, but it does change the dynamics for the Fed.

The markets are eager for the first rate cut, but the data dependency of the Fed is making it tough to stay on the projected path of two to three cuts this year. We would prefer the Fed act when there is clear confirmation of sustainably lower inflation instead of risking an overheated scenario. It’s reasonable to assume the Fed is acutely aware of the double inflation top of the 1970s and is not interested in seeing double inflation for itself. The good news is that high policy rates will continue to create opportunities in the bond market, and current rate levels are attractive as an entry point for our clients comfortable with extending maturities. Given a consensus that the 10-year U.S. Treasury yield will fall before the end of 2024, we have high conviction it’s a good trade.

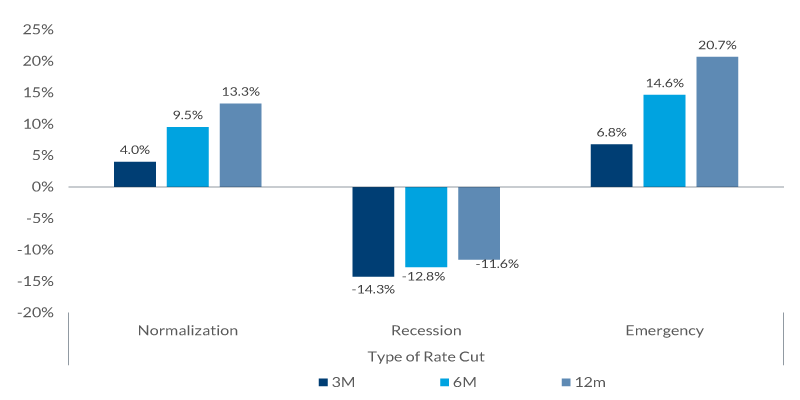

What is very clear to us is that the Fed is done hiking interest rates. The big picture is still one in which monetary policy will become looser over the next 12 months, a helpful force for the economy and financial markets. Stock market performance is influenced by the stance of the Fed and, when rates are being normalized as opposed to being slashed in an emergency, stocks tend to do well. Going back to 1984, when rates were cut as part of a normalization process, the S&P500 rose 13.25% on average. There is a strong case that the equity market can continue to move higher, but at current valuations and with a more patient Fed, scrutiny of the current run is intensifying.

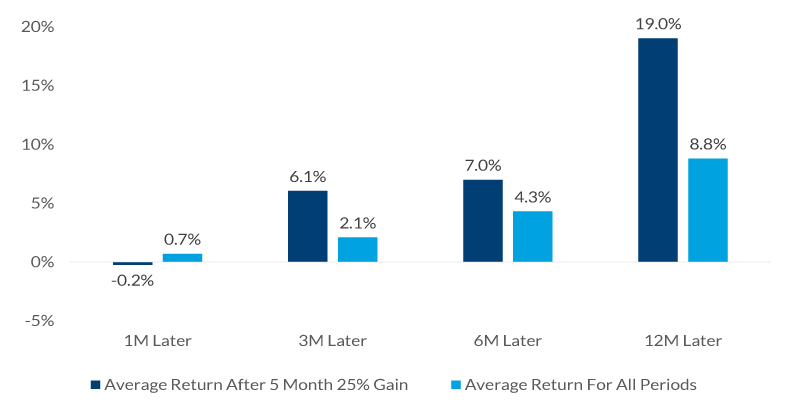

Over the past five months, the S&P500 is up 25.3%, which is the seventh time the index has gained more than 25% since WWII over a five-month span. The near-term historical experience is mixed and over one-month periods after hitting peak returns, the market has been essentially flat. However, over 12 months, the average return is 21.1%. So, it wouldn’t be out of the ordinary to see a decline in the market, especially in light of the intensifying geopolitical conflicts, but we believe investors should stay the course and use any significant pullbacks as an opportunity to add to equity exposure. While we can’t ignore the elevated anxiety over what’s happening globally, a sustained selloff in stocks is much more likely to be caused by a U.S. domestic economic problem than an international war.

Chart 2: S&P 500 Performance

After First Fed Rate Cut

Sources: FactSet, St. Louis Fed, as of April 2024.

Information is subject to change and is not a guarantee of future results.

Still, valuation is quite high at over 21x, and the biggest risk to the market is likely twofold. First, any unwind of earnings expectations or a stumble during earnings season could result in a move lower. Second, the current level of interest rates will eventually become a headwind, especially if the Fed stays on hold. With very high expectations, earnings growth will need to come through to justify extended valuations; at market consensus above 11% for FY2024, there’s quite a bit of downside to the estimates and limited upside. Given the amount of the liquidity that came into the market during the pandemic, the increase in rates has not been felt fully, but that clock is ticking. Together with rising geopolitical risk, it’s very likely that we will see a stumble or two this year.

Chart 3: S&P 500 Performance

Source: Ned Davis Research, as of February 2024.

Indices are unmanaged, and one cannot invest directly in an index. Index returns do not reflect a deduction for fees or expenses.

Past performance is no guarantee of future results.

But we think we’re ready for this. While our defensive exposure has come down, our core equity portfolio remains focused on quality, holding reasonably valued companies with strong fundamentals and growth prospects. For clients seeking additional capital appreciation, we’ve increased exposure to mid- and small-cap companies, which have lagged the rally but should benefit from improved confidence in the economic outlook and a broadening in market participation. History also suggests dividend stocks are attractively priced, and dividend growth can provide more income-oriented investors with the potential for a hedge against inflation.

In Fixed Income, we have yet to materially extend duration on a relative basis, but we are just fine with benchmark duration. The key is for investors with long-term time horizons and income needs to take the plunge into longer maturity strategies, especially if they are holding cash. While price appreciation in bonds may be limited until inflationary pressures abate, yield levels on high-quality fixed income continue to provide attractive opportunities. In fact, this is the first time in many years that investors have been able to take advantage of a divergence in asset classes. We see a rich set of opportunities across the bond market that was previously only a pipe dream two years ago.

Given the current economic advantages, asset allocation options and higher rates, we do expect positive returns to continue for well-balanced portfolios. However, going forward we expect more modest returns, and we are positioning portfolios to remain durable in an environment with structurally higher interest rates. As investors reset expectations within a longer-term market advance, more divergence is likely, which will demand greater flexibility and active management with an opportunistic approach to take advantage of any dislocations the market offers. We will be looking for such opportunities at some point in the months ahead to add quality investments to portfolios, as well as to think about diversifying portfolios for a potential broadening of market leadership.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations,estimates, projections, and other forward-looking statements are based on available information and management’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification may not protect against market risk or loss. Past performance is no guarantee of future performance.

There are inherent risks with equity investing. These risks include, but are not limited to stock market, manager, or investment style. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

There are inherent risks with fixed income investing. These risks may include interest rate, call, credit, market, inflation, government policy, liquidity, or junkbond. When interest rates rise, bond prices fall.

Index Definitions

S&P 500 Index: The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the US It is not an exact list of the top 500 US companies by market cap because there are other criteria that the index includes.

Non-deposit investment Products are: • not FDIC insured • not Bank guaranteed • may lose value

© 2024 City National Bank. All rights reserved.

Stay Informed.

Get our Insights delivered straight to your inbox.

Read more of this month's Quarterly Update below:

Put our insights to work for you.

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.