Insights

Tax-Exempt Strategies:

Municipals Bounce but Stay the Course

Key Points

- Absolute yields tick higher, underscoring long-term value.

- Supply deficit and ample liquidity propel high-yield prices.

- Credit fundamentals benefit from extended economic glide path.

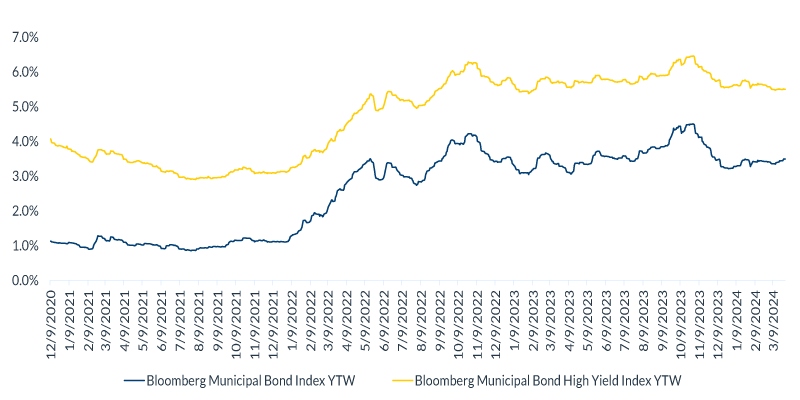

Municipal bonds carefully confronted financial market volatility to deliver favorable relative performance to begin the year. Notwithstanding the whipsaw in rates, Bloomberg indices reported investment-grade (IG) municipal bonds posted a slightly negative return of 39 bps for the quarter, while high-yield municipals (HYM) rewarded their investors with a 1.5% total return. To give perspective, U.S. Treasuries closed out the first quarter in the red 96 bps. The comparatively strong showing of IG and HYM bonds is attributable to solid investor demand, as evidenced by positive net municipal mutual fund flows YTD of nearly $8 billion and the favorable impact of income accrual on fluctuating bond prices. Absolute municipal bond yields remain a linchpin to their value proposition for long-term investors seeking attractive tax-efficient cash flow and forward-return potential. According to Bloomberg indices, IG and HYM index yield-to-worst (YTW) settled at 3.5% and 5.5%, respectively, at quarter-end, translating into taxable-equivalent yields1 of 5.9% and 9.3%, respectively. Municipal bonds historically benefit from a lower correlation to other asset classes, which tends to reduce portfolio volatility over time, thus currently available yields offer a compelling entry point for investor portfolios.

Chart 1: Yield-to-Worst (YTW) for IG and HYM Bonds Remain Attractive

Source: Bloomberg, as of March 29, 2024.

All sources are Bloomberg indexes.

Indexes are unmanaged and do not reflect a deduction for fees or expenses. Investors cannot invest directly in an index. Information is subject to change and is not a guarantee of future results.

Technical factors often play a significant role in the price behavior of municipal bonds. Gross issuance reached approximately $100 billion during the quarter, or a 25% increase YoY. Despite the strong trend of municipal market supply, deal flow in the HYM space underwhelmed demand. The lack of traditional HYM supply has bolstered liquidity and improved secondary market trading conditions as product scarcity benefited security prices. Moreover, as the probability of an economic correction this year dissipates, HYM investors have become more comfortable with risk. Credit spreads, as measured by the YTW differential of the Bloomberg Municipal High Yield Index relative to the Bloomberg Municipal (IG) Index AAA and BBB YTW, have declined since the beginning of the year by approximately 40 bps and 15 bps, respectively. These trends are likely to continue in the near term; however, dislocation in the Treasury market or changes in expectations for Fed policy could have implications. With the perceived belief that the rate cycle has likely plateaued, longer-duration assets have garnered increased attention, contributing to the favorable first-quarter performance.

Chart 2: 1Q 2024 Fixed Income Asset Class Returns

Source: Bloomberg, as of March 29, 2024.

All indices used in the chart above are Bloomberg.

Past performance or performance based upon assumptions is no guarantee of future results. Indexes are unmanaged and do not reflect a deduction for fees or expenses. Investors cannot invest directly in an index. Information is subject to change and is not a guarantee of future results.

The resilient economy continues to underpin municipal credit conditions. Moody’s reported a third consecutive year of upgrades outpacing downgrades in 2023. Reserve funds of state and local governments remain at or near record levels, while many revenue enterprises have either reached or exceeded their pre-pandemic operations. Should budget performance decelerate or turn negative, most issuers are well-positioned to manage through a period of instability. Within HYM, troubled borrower activity remains in line with the quarterly experience of last year, with continued pressure in a few sectors, like senior living, albeit trends are beginning to improve in some regions. Credit selectivity, security structure, and sector orientation are key considerations in navigating the market.

1Taxable-equivalent yield – this is based on 37% marginal + 3.8% Medicare Surcharge

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations,estimates, projections, and other forward-looking statements are based on available information and management’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification may not protect against market risk or loss. Past performance is no guarantee of future performance.

There are inherent risks with equity investing. These risks include, but are not limited to stock market, manager, or investment style. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

There are inherent risks with fixed income investing. These risks may include interest rate, call, credit, market, inflation, government policy, liquidity, or junkbond. When interest rates rise, bond prices fall.

Bloomberg risk is the weighted average risk of total volatilities for all portfolio holdings. Total Volatility per holding in Bloomberg is ex-ante (predicted) volatility that is based on the Bloomberg factor model.

Municipal securities. The yields and market values of municipal securities may be more affected by changes in tax rates and policies than similar income-bearing taxable securities. Certain investors’ incomes may be subject to the Federal Alternative Minimum Tax (AMT), and taxable gains are also possible. Investments in the municipal securities of a particular state or territory may be subject to the risk that changes in the economic conditions of that state or territory will negatively impact performance. These events may include severe financial difficulties and continued budget deficits, economic or political policy changes, tax base erosion, state constitutional limits on tax increases and changes in the credit ratings.

Index Definitions

Bloomberg Municipal Bond Index: The Bloomberg US Municipal Bond Index measures the performance of investment grade, US dollar-denominated, long-term tax-exempt bonds.

Bloomberg Municipal High Yield Bond Index: The Bloomberg Municipal High Yield Bond Index measures the performance of non-investment grade, US dollar-denominated, and non-rated, tax-exempt bonds.

S&P Leveraged Loan Indexes (S&P LL indexes) are capitalization-weighted syndicated loan indexes based upon market weightings, spreads and interest payments. The S&P/LSTA Leveraged Loan 100 Index (LL100) dates back to 2002 and is a daily tradable index for the US market that seeks to mirror the market-weighted performance of the largest institutional leveraged loans, as determined by criteria. Its ticker on Bloomberg is SPBDLLB.

Bloomberg US Corporate Bond Index: The Bloomberg Barclays US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

Bloomberg US High Yield Index: The Bloomberg US Corporate High Yield Index measures the performance of non-investment grade, US dollar-denominated, fixed-rate, taxable corporate bonds.

Bloomberg Investment Grade Index: The Bloomberg US Investment Grade Corporate Bond Index measures the performance of investment grade, corporate, fixed-rate bonds with maturities of one year or more.

Investment Grade (IG) Municipal Bond Index: The Bloomberg US Municipal Bond Index measures the performance of investment grade, US dollar-denominated, long-term tax-exempt bonds.

High Yield (HY) Municipal Bond Index: The Bloomberg Municipal High Yield Bond Index measures the performance of non-investment grade, US dollar-denominated, and non-rated, tax-exempt bonds.

Non-deposit investment Products are: • not FDIC insured • not Bank guaranteed • may lose value

Stay Informed.

Get our Insights delivered straight to your inbox.

More from the Quarterly Update

Put our insights to work for you.

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.