Insights

Tax-Exempt Strategies:

Municipals Grind Higher With the Finish Line in Sight

- Asset class performance are currently comfortably “in the green.”

- Absolute yields continue to attract investor capital.

- Credit fundamentals are normalizing but remain durable.

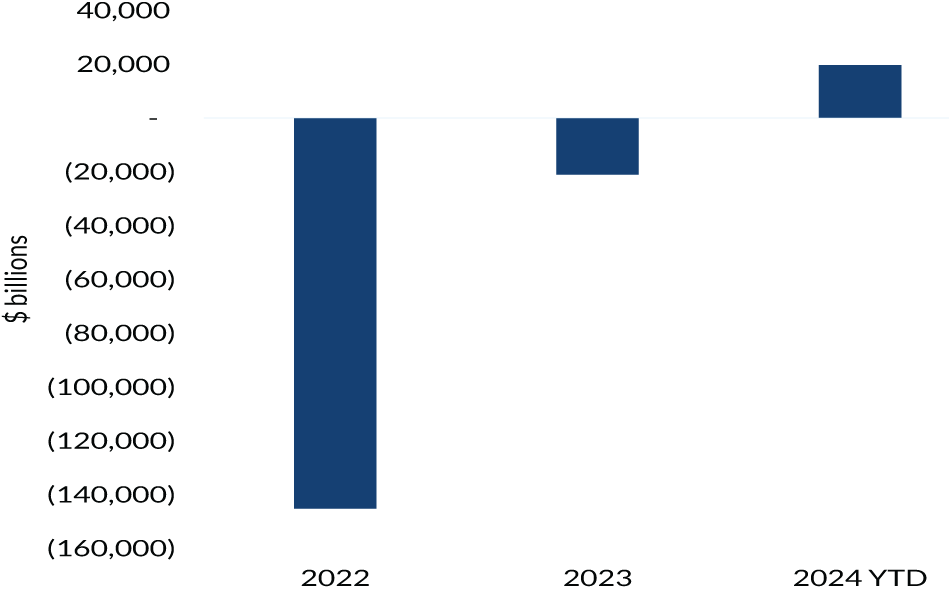

Municipal bonds closed out the third quarter in fashion as investment-grade (IG) and high-yield (HYM) bonds posted solid performance, with July and August monthly returns positive for the first time since 2020. On the year, the Bloomberg Municipal Bond Index and the Bloomberg Municipal High Yield Bond Index have rewarded their investors with 2.2% and 7.4% gains, respectively, through 3Q20241. In a trend that has increasingly improved since record outflows from municipal bond mutual funds during 2022, net inflows have continued to gain ground fairly consistently, particularly for HYM bonds. Coupled with cash on the sidelines that had remained somewhat dormant since last year amid rate volatility and an uncertain economic trajectory, the demand side of the market has benefitted the asset class YTD despite the strength in bond supply.

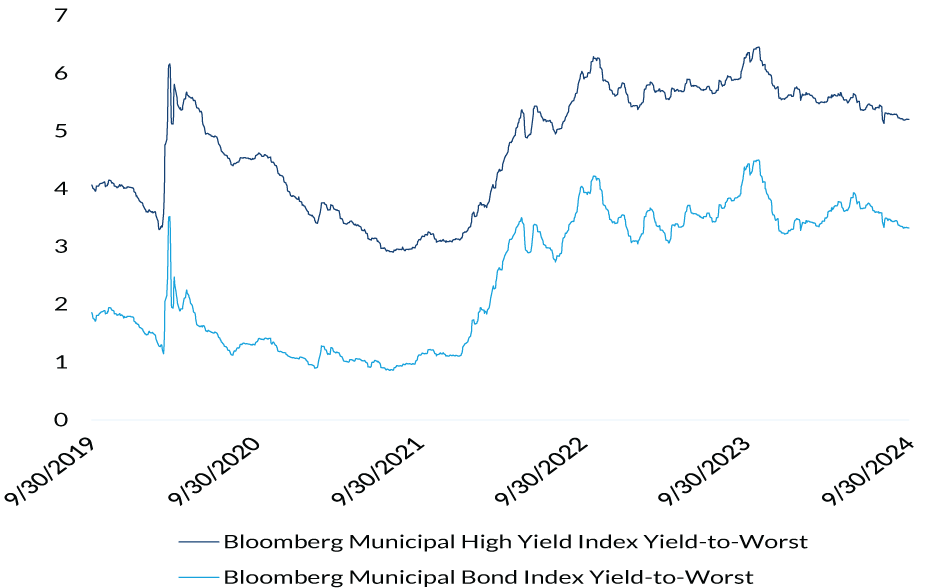

Chart 1: Municipal Bond Yields Remain Attractive

Source: Bloomberg, as of September 30, 2024.

Indexes are unmanaged and do not reflect a deduction for fees or expenses. Investors cannot invest directly in an index.

Information is subject to change and is not a guarantee of future results.

Bloomberg gross municipal bond sales through 3Q2024 of about $360 billion are approximately 40% higher vs. 2023, and on track to surpass recent years’ high-water mark. From a purely yield perspective, the technical strength of the market has not materially altered the attractiveness of municipal bonds. As of quarter-end, absolute yields, per Bloomberg, for IG and HYM bonds of 3.3% and 5.2%, respectively, equate to a taxable equivalent basis of more than 5.5% and 8.75%, respectively1. We believe long-term investors have an opportunity to take advantage of attractively priced cash flows in the current environment, especially given the improvements in bond valuations since the end of 2Q2024 (i.e., the ratio of municipal bond yields vs. comparable Treasury maturities has increased, which signals increasing value to municipal investors).

With the Fed recently beginning its easing cycle, the economy is forecast to moderate, but municipal bond quality is well-positioned at this time. Credit spreads have generally declined since the beginning of the year and remain somewhat tight to recent years’ levels. As Election Day approaches, credit spreads are anticipated to remain range-bound, but should economic data soften beyond expectations, lower quality bonds are more vulnerable to widening. Municipal credit is transitioning back into equilibrium as operating risks come more into balance with normalizing revenues (necessitating spending adjustments). Balance sheet liquidity and reserve funds remain sound, however, which will provide an important buffer for most issuers confronting challenges. We are also closely monitoring the outcomes of national, state, and local elections and their potential policy implications, such as tax reform or sector-specific considerations.

Chart 2: Cumulative Flows (in $b)

Source: Bloomberg ICI Municipal Bond Estimated Weekly Net New Cash Flow, as of September, 30 2024. Indexes are unmanaged and do not reflect a deduction for fees or expenses.

Information is subject to change and is not a guarantee of future results.

1 Bloomberg, as of September 30, 2024.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations,estimates, projections, and other forward-looking statements are based on available information and management’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification may not protect against market risk or loss. Past performance is no guarantee of future performance.

There are inherent risks with equity investing. These risks include, but are not limited to stock market, manager, or investment style. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

There are inherent risks with fixed income investing. These risks may include interest rate, call, credit, market, inflation, government policy, liquidity, or junkbond. When interest rates rise, bond prices fall.

Bloomberg risk is the weighted average risk of total volatilities for all portfolio holdings. Total Volatility per holding in Bloomberg is ex-ante (predicted) volatility that is based on the Bloomberg factor model.

Municipal securities. The yields and market values of municipal securities may be more affected by changes in tax rates and policies than similar income-bearing taxable securities. Certain investors’ incomes may be subject to the Federal Alternative Minimum Tax (AMT), and taxable gains are also possible. Investments in the municipal securities of a particular state or territory may be subject to the risk that changes in the economic conditions of that state or territory will negatively impact performance. These events may include severe financial difficulties and continued budget deficits, economic or political policy changes, tax base erosion, state constitutional limits on tax increases and changes in the credit ratings.

City National Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

© 2024 City National Bank. All rights reserved.

Index Definitions

S&P 500 Index: The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the US It is not an exact list of the top 500 US companies by market cap because there are other criteria that the index includes.

The MSCI EAFE Index is a stock market index that measures the equity market performance of developed markets outside of the U.S. & Canada.

DJ US Select Dividend Index: The Dow Jones U.S. Select Dividend Index aims to represent the U.S.’s leading stocks by dividend yield.

Bloomberg Municipal Bond Index: The Bloomberg US Municipal Bond Inde x measures the performance of in vestment grade, US dollar-denominated, long-term tax-exempt bonds.

Bloomberg Municipal High Yield Bond Inde x: The Bloomberg Municipal High Yield Bond Inde x measures the performance of noninvestment grade, US dollar-denominated, and non-r ated, tax-exempt bonds.

Bloomberg Investment Grade Index: The Bloomberg US In vestment Grade Corporate Bond Index measures the performance ofinvestment grade, corporate, fixed-rate bonds with maturities of one y ear or more.

G0BA Index: ICE BofA US Treasury Bill Index:The index measures the performance of US dollar denominated US Treasury Bills publicly issued in the US domestic market. Qualifying securities must have at least one month remaining term to final maturity and a mini mum amount outstanding of $1 billion. It is capitalization-weighted.

G0Q0 Index: ICE BofA US Treasury Index: ICE BofA US Treasury Bill Index:The index measures the performance of US dollar denominated US Treasury Bills publicly issued in the US domestic market. Qualifying securities must have at least one month remaining term to final maturity and a minimum amount outstanding of $1 bi llion. It is capitalization-weighted.

LUACTRUU Index: Bloomberg US Corporate Total Return Value Unhedged USD: The Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

LF98TRUU Index: Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD. Bloomberg: LF98TRUU Index: The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fi xed-rate corporate bond market.

Securities are classifi ed as high yield if the middle rati ng of Moody’s, Fitch and S&P is Ba1/BB+/BB+or below. Bonds from issuers with an emerging markets country of risk, based onBloomberg EM country defi niti on, are excluded. This is the total return index level.

Indexes are unmanaged and do not reflect a deduction for fees or e xpenses. Investors cannot invest directly in an index.

Definitions

Yield to Worst (YTW) is the lower of the yield to maturity or the yield to call. It is essentially the lowest potential rate of return for a bond, excluding delinquency or default.

P/E Ratio: The price-to-earnings ratio (P/E ratio) is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

The 4P analysis is a proprietary framework for global equity allocation. Country rankings are derived from a subjective metrics system that combines the economic data for such countries with other factors including fiscal policies, demographics, innovative growth and corporate growth. These rankings are subjective and may be derived from data that contain inherent limitations. MSCI Emerging Markets Asia Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the Asian emerging markets.

The Magnificent Seven stocks are a group of high-performing and influential companies in the U.S. stock market: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla.

City National Rochdale Proprietary Quality Ranking formula: 40% Dupont Quality (return on equity adjusted by debt levels), 15% Earnings Stability (volatility of earnings), 15% Revenue Stability (volatility of revenue), 15% Cash Earnings Quality (cash flow vs. net income of company) 15% Balance Sheet Quality (fundamental strength of balance sheet).

*Source: City National Rochdale proprietary ranking system utilizing MSCI and FactSet data. **Rank is a percentile ranking approach whereby 100 is the highest possible score and 1 is the lowest. The City National Rochdale Core compares the weighted average holdings of the strategy to the companies in the S&P 500 on a sector basis. As of September 30, 2022. City National Rochdale proprietary ranking system utilizing MSCI and FactSet data.

BPS: A basis point (BPS) is used to indicate changes in the interest rates of a financial instrument. Basis points are typically expressed with the abbreviations “bp,” “bps,” or “bips.”

A consensus estimate is a forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Bureau of Labor Statistics(BLS): The BLS is a federal agency that collects and disseminates important information about labor, wages, prices, and productivity.

© 2024 City National Bank. All rights reserved.

Non-deposit investment Products are: • not FDIC insured • not Bank guaranteed • may lose value

Stay Informed.

Get our Insights delivered straight to your inbox.

More from the Quarterly Update

Put our insights to work for you.

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.